Where is the power battery industry going?

Where is the power battery industry going? After playing these three hard games, you will know.

Recently, the IPO of Ningde era has passed smoothly.

When focusing on the keywords such as "Fujian's richest man", "100 billion worth", "lightning over", few people will notice that Ningde era from the industry's third in 2016, one by one, BYD and Panasonic jumped away The industry boss has only spent more than a year.

So what did the Ningde era do?

In addition, the current general situation of the domestic power battery industry, in a word is: "The boss is a sudden rise, the second child fell to the throne, the wolves compete for the third." In addition to the surface policy, market, technical route changes, what are the key development stages And the elements, even the "battle", contributed to this pattern? How will the future trend develop?

This article attempts to answer these questions.

Boss riding a dusty second child to catch upLast week, the IPO of Ningde era successfully passed the meeting, set a record of 24 days of lightning over A shares, and the listing value of 130 billion, the first share of the power battery in the listing speed and valuation.

Behind the "first stock" reputation is the rapid growth in performance in the Ningde era.

Data show that in 2016, the Ningde era's power battery shipments were 6.72GWh, ranking third in the global rankings after Panasonic and BYD. By 2017, the shipment of power batteries in the Ningde era increased by 73% to 11.8GWh, surpassing Panasonic in one fell swoop and winning the first place in the industry. This data change took only one year.

Judging from the installed capacity of power batteries reflecting market share, the installed capacity of power batteries in Ningde era in 2017 was 10.4GWh, and one of the exclusive 30% market, supporting more than 500 models of passenger cars and passenger cars.

In 2016, the power battery was the first in the country, and BYD, the second in the world, suffered from Waterloo in 2017 with the sudden emergence of the Ningde era. In 2016, BYD's power battery shipments were 7.35GWh. By 2017, its installed capacity dropped to 5.4GWh. When the industry as a whole developed rapidly, its performance did not increase.

The market of BYD's power battery was robbed by the Ningde era!

But in this market, the Ningde era has been well-founded.

In China, BYD is one of the first car companies to develop lithium iron phosphate power batteries, and BYD has been clearly supporting the lithium iron phosphate flag before the national policy in 2016. BYD has enjoyed this benefit for a long time. Before 2016, BYD not only supplied lithium iron phosphate batteries for its new energy passenger cars and buses, but also supplied batteries for other bus companies. By the new energy bus in the country to promote the first, the amount of subsidies is huge, plus the self-contained passenger car business, BYD became the industry's first.

But after 2016, the style of painting changed suddenly. At that time, the new energy vehicle fraud incident broke out, the bus market became the hardest hit area, and then the policy hit hard to crack down on the subsidy, the new energy vehicle subsidy began to decline in 2017, seeking to withdraw. Affected by this, the new energy bus industry suffered a setback in 2017. The annual sales volume (about 85,000 vehicles) decreased by more than 20,000 vehicles compared with 2016. The demand for power batteries for passenger cars also declined. BYD was unfortunately lying down and its business was shrinking.

It is worth mentioning that the Ningde era was actually the largest supplier of lithium iron phosphate batteries for passenger cars in 2016, but it seems that it has not been affected.

Because the Ningde era has a ternary lithium card. In the 2017 sales share of Ningde era, ternary lithium batteries accounted for nearly half. In the Ningde era, which is homologous to the consumer lithium giant ATL (mainly producing lithium cobalt oxide battery), it is more familiar with the ternary lithium system and its layout is earlier.

After 2015, the country began to recognize the safety of ternary lithium materials for vehicle batteries. After the policy was loosened, the energy density was higher, and the ternary lithium battery, which represents a farther battery life, began to dominate the passenger vehicle market. Beiqi New Energy's EX and EU series, Geely Emgrand EV, and SAIC Roewe ERX5, including Tesla's new energy vehicles, which are named after you, are basically fans of ternary lithium batteries.

Roewe ERX5, using Ningde era ternary lithium battery

In 2017, the domestic production of new energy passenger vehicles reached 478,000, an increase of more than 200,000 units from the previous year. In the downturn of the new energy bus market, new energy passenger cars that continue to triumph have become the core of the growth of power battery performance. However, BYD is limited by the technical route choice, and it is too late to follow up the ternary lithium; on the other hand, because BYD's battery only supplies its own vehicles in the passenger car market, it has not eaten this market dividend at all. One to two, the rise of Ningde era, BYD fell to the throne, becoming the theme of the 2017 power battery industry.

The policy and technology routes suddenly turned over, and BYD, who had insufficient reserves, was caught off guard. With painstaking thoughts, BYD began to change in business and offered two moves.

BYD's first move is actually not too late. Starting in 2017, BYD began to embrace ternary lithium in its passenger car business. In the first half of the year, BYD launched the hybrid models Tang 100 and Qin 100, and the batteries used in the vehicles were all ternary lithium. After the test was completed, BYD also applied ternary lithium on its pure electric models, the Song EV 300 and the Qin EV 300. And this year, BYD said that the future pure electric models will use ternary lithium batteries. A new generation of new energy vehicles that once died of lithium iron phosphate,

BYD Tang 100

But the more crucial second move, BYD is still in the process of preparing for the separation of the power battery business and supplying it to other new energy vehicles. This move, BYD power battery in the passenger car market, potential customers, will be several times the original. According to Shen Wei, deputy general manager of BYD's lithium battery division, the power battery business will be split at the end of 2018 or early 2019 and is expected to be listed within five years.

In the Ningde era has already won the market share of nearly 30% of domestic power batteries - when BYD is doubled, how will BYD's change will challenge the new hegemon of Ningde era, whether it can return to the first, it will be the future Chinese power battery One of the most interesting dramas.

Fight for the third person, the third world is fightingWhen the boss of the industry just swapped the position, the "third world" of China's power battery is trying to compete for the third place. Compared with the rapid development of the Ningde era and the deep accumulation of BYD in one year, these companies lack the persuasive power of the top two in terms of volume - the largest of which is Walter, the installed capacity in 2017 is only 2.3GWh. .

The sense of crisis in the domestic power battery companies is undoubtedly deep, because BYD, which was the leader last year, was opened up in the Ningde era. Backwaters, which is backed by listed company Jianrui Woneng, is no exception. This company is ranked fourth with the same listed company last year. Guoxuan Hi-Tech, which is listed company, has a gap of 0.4GWh in the installed capacity of lithium batteries. The power battery is under construction at a fraction of the capacity - Waterma's planned capacity in 2020 is 20GWh, while Guoxuan Hi-Tech's target is higher, 30GWh. Under the ultra-high production capacity, any company's production line can cover the performance of the current year as long as it is driven for one month. Of course, the premise is that it can get so much market share.

In 2017, the power battery installed capacity of companies such as BAK, Feneng, and Zhihang did not exceed 2GWh, but their performance showed super high growth – because they are all specializing in ternary lithium. Power battery production, with the opportunity of ternary lithium in the passenger car market in 2017 staged a doubling of shipments, of which the shipments of Zhihang increased nearly 10 times compared with 2016.

In this dramatic market, no one in the industry's third position can say that he is sitting down. But the third position is actually becoming the focus of domestic power battery companies: China's manufacturing industry is becoming more and more like China's Internet companies - only the first two of the industry can survive - or slightly better, can survive the top three name.

The national will and commercial capital are joining forces, and resources are increasingly concentrated in the first echelon. For the potential juniors in the power battery industry, this is not only a battle of performance, but also a battle between life and death.

Industry situation: the differentiation of passenger cars and bus batteries has been determinedAnother major trend in the field of power batteries in 2017 is that the power battery technology routes adopted in different new energy vehicles have begun to differentiate and be fixed. Overall, this trend is that new energy passenger cars are biased towards ternary lithium, while new energy buses use lithium iron phosphate, and new energy special vehicles (trucks) are also more inclined to use ternary lithium.

From the data point of view, in 2017, the new energy passenger car ternary lithium battery installed machine accounted for 76%, the special car accounted for 69%, and the new energy bus as much as 90% of the share is occupied by lithium iron phosphate .

The high energy density of ternary lithium and the ability to provide longer battery life is a consensus in the industry. By 2017, the price of ternary lithium battery packs has dropped to a minimum of 1.4-1.5 yuan/Wh, which is basically the same as lithium iron phosphate. The price advantage of lithium iron phosphate is no longer the same, and the energy density is at a disadvantage. Why do new energy buses still stick to this type of battery?

After talking with senior practitioners in the power battery industry, we got a more rigorous answer: Lithium iron phosphate power battery is much higher than the ternary lithium battery in high temperature safety and collision, puncture safety, for a large number of people involved, For public safety buses, the priority of safety performance is much higher than the cruising range. Moreover, since the ternary lithium battery requires a steel casing and a more complicated cooling system protection, the energy density does not split the lithium iron phosphate too far after the battery system is formed, but in the theoretical energy density, the ternary lithium has more Large development space.

Based on the safety priority and the performance characteristics, the new energy bus chose lithium iron phosphate. Even in the Ningde era, which tasted the sweetness of the ternary lithium battery business, it also said that the lithium iron phosphate battery will still be a new energy for quite some time. The best choice for passenger cars.

New energy bus, lithium iron phosphate battery is widely used

The endurance is a passenger car with a greater pain point, and the corresponding ternary lithium battery is selected. At present, due to the legacy of the existing technical route selection, there are many new energy passenger vehicles, especially hybrid vehicles that use lithium iron phosphate batteries. However, with the iron-iron supporter of the lithium iron phosphate, BYD has turned to ternary lithium, the future share of the ternary lithium battery in the passenger car market is only inevitable.

As for other types of power batteries, such as lithium manganate and lithium titanate, which have been marginalized in the big waves, it is likely to become a footnote in the history of new energy vehicles.

For example, the AESC, which once used lithium manganese oxide batteries for Nissan Leaf, has been transferred to the ternary lithium battery route after being acquired by Chinese capital Jinshajiang Capital. And Zhu Dong Yinlong, who is determined to do it, produces lithium titanate batteries with a market share of only 4% in the new energy bus market.

Of course, with the further development of technology in the future, there may be variables in the differentiation of the new energy passenger car and bus market. For example, the safety performance of the ternary lithium battery has reached a new level, and the status of lithium iron phosphate in the passenger car market continues. challenge. But so far, or the consideration of security attributes, or the results of various parties' games, ternary lithium corresponds to passenger cars + special vehicles, and the situation of lithium iron phosphate corresponding to passenger cars is relatively stable.

Three wars of power batteryHowever, the technical route of the power battery has come to an end, just ending (or suspending) the first war in the industry. In this rapidly expanding sunrise industry, three comprehensive wars have started at the same time.

1. The battle of scale

In November 2016, the Ministry of Industry and Information Technology issued a public consultation draft “Automobile Power Battery Industry Standard Conditions (2017)â€, which directly increased the capacity requirements (single cells) of power battery companies to 8GWh. The "Industry Code" is a white list of power batteries. In order to enter the new energy vehicle subsidy list, 8GWh overnight becomes the red line of life and death of power battery companies.

The ministry's consideration was that at that time, the power battery industry had already produced more than 200 battery companies in the era of large subsidies, forming too much backward capacity and small production capacity. However, from the international situation, this is the power to disperse China's power battery.

Because the competition in the automotive industry has long been a global competition, foreign participation is one of the few giants in each country, and the power battery industry is the same. Overseas, Panasonic is Japan's power battery leader, LG and Samsung are South Korea's power battery duo. They are huge in size and they are taking advantage of scale and are leading the way in battery technology and automation.

To make China's power battery go to the international market, it is a must to integrate a power battery giant that can compete with Panasonic LG Samsung. Therefore, China has resorted to policy tools to promote the power battery industry to low-capacity and backward production capacity with extremely high production capacity standards, and encourage mergers and acquisitions and advantageous enterprises to become bigger and stronger. The "Industry Code" was born.

However, this opinion draft came out and the industry was at a loss. Because at that time, the conditions were met, only BYD and Ningde era. Later, the news that the red line will be lowered to 3-5GWh, but until today, this opinion draft has not been officially released. After all, it involves too many power battery companies to live and die, and the benefits involved are too deep.

While the companies complained, they were desperately working on the production capacity, and staged the life-and-death speed of the power battery industry – meeting the 8GWh capacity standard before the official introduction.

Only in 2017, the public information shows that Ningde era plans to expand to 50GWh in 2020, BYD will expand to 26GWh in 2018, Tianjin Lishen will expand to 20GWh in 2020, and Yiwei Lithium will expand to 9GWh in 2017, Far East Volkswagen expanded to 22GWh in 2018, and Waterma expanded to 20GWh in 2017. These total a total of 147GWh, and this is only a part of more than 200 power battery companies. According to the "Action Plan for Promoting the Development of Automotive Power Battery Industry" issued by the four ministries and commissions of the Ministry of Industry and Information Technology in March 2017, the state plans to form a power battery capacity of 100 billion watt-hours, or 100 GWh, by 2020. However, only the capacity planning of some enterprises now has a surplus of nearly 50%.

Huxi production base in the construction of Ningde era

The original capacity-removal policy, under the mad competition, eventually formed a new round of capacity competition and even capacity war. The interaction between market and policy, the dual relationship between central will and local power, is played in the battle of the scale of power battery companies.

Of course, power battery companies have expanded their production capacity. In addition to the policy drive, on the other hand, they also realized that the scale effect will be one of the key points for the next cost battle.

2, the battle of cost

Also in the "Promoting Action Plan for the Development of Automotive Power Battery Industry", the state has put forward a request that by 2020, the price of the power battery system will reach 1 yuan/Wh, which is 1,000 yuan per kilowatt hour (KWh).

According to this standard, the cost of new energy vehicles with a 50KWh battery and a battery life of more than 300 kilometers (excluding some 7 large SUVs) will drop to 50,000 yuan. The current price is, according to the information disclosed in the Ningde Times prospectus, the price of its power battery system is 1.4 yuan / Wh (this is still the quotation of the industry leader), in the above example, the battery cost of the model reached 70,000 yuan, the difference Reached 20,000 yuan.

If the difference of 20,000 yuan is reflected in the price, this is enough to affect a large number of consumers, especially in the market of affordable models, so as to further promote new energy vehicles.

In fact, the price war in the power battery industry has already started for a long time. Taking Ningde era as an example, the average sales price of power battery systems in the three years from 2015 to 2017 was 2.28 yuan/Wh, 2.06 yuan/Wh and 1.41 yuan/Wh. In 2017, the price of its power battery system was reduced by 0.65 yuan per Wh - the battery of one degree was reduced by 650 pieces. In contrast, the unit cost of the power battery system in the Ningde era in the past three years was 1.33 yuan/Wh, 1.13 yuan/Wh and 0.91 yuan/Wh, respectively. Although it also showed a downward trend, the speed of cost reduction was significantly lower than the rate of price decline.

Average sales price of power battery system in Ningde era 2015-2017

The scale effect brought about by the rapid expansion of the Ningde era has contributed. Various power battery companies have already learned this trick.

In addition to the main approach to scale, the players in the power battery industry have adopted methods to reduce the level of automation and adopt modular design.

A further way to play is to extend the sphere of influence beyond the power battery. BYD is the representative of this path. In the downstream of the power battery industry chain, BYD has its own vehicle business; in the upstream of the industry chain, BYD invested 245 million in 2017 to set up a new company in Qinghai to develop lithium resources. Coincidentally, the Ningde era also controlled Guangdong Bangpu in the downstream, involved in the power battery recycling business, in the upstream Ningde era, recently acquired Canada's North American lithium industry, involved in lithium mine development. By opening up the closed loop of business in the upstream and downstream of the industry chain, it is becoming a popular game for power battery giants to reduce costs.

In addition, it is also important to step up research and development in technology to increase product yield and product energy density (and thus reduce the price in disguise under the same parameters).

However, for all power battery players, there are currently two factors that are bothering them.

First, the price of raw materials for power batteries has skyrocketed. Taking the most expensive cathode material, cobalt, for example, the price per ton of cobalt has exceeded 600,000 yuan, and it is still growing at an average price of nearly 10% per month. The name "cobalt grandma".

The second factor is the unique problem of China's power battery companies - state subsidies are declining, and it is expected that by 2020, new energy subsidies will be fully withdrawn. Competition with international giants without subsidies will be a major test for domestic power battery companies.

3, the battle of performance

In addition to the battle between cost and scale, power battery companies are also facing the most test of internal strength.

In the Action Plan, the national policy sets a target of 260 mah/g for the power battery system in 2020. At present, the domestic energy battery system that has been commercialized has a maximum energy ratio of just over 140 mah/g, and this target has a huge gap.

The latest power battery system built by Panasonic and Tesla, using 2170 cylindrical battery form and NCA (nickel cobalt lithium aluminate) positive + carbon silicon negative electrode, it is estimated that its specific energy is close to or reaches 200mah level, and Commercialized applications are implemented on Model 3.

Tesla 2170 battery

Compared with international giants, there is still a big gap in the domestic energy battery system in terms of energy density. For this problem, a classic tactic of domestic enterprises is: learning to follow up advanced foreign experience.

BAK, Yiwei Lithium and Lishen are all building their own 2170 battery production lines, while Ningde Times and other companies have invested in the research and development of carbon-silicon anodes, and Lishen has added the RCA technology route.

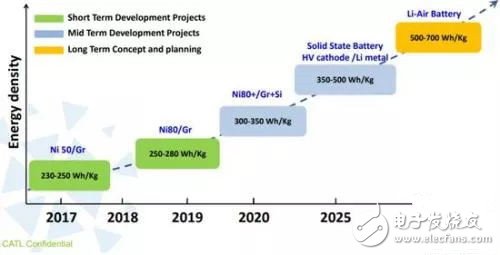

Ningde era power battery performance research and development plan (Note: the energy density in the figure is a single cell instead of the system; planning time 2017-2023)

In addition, perhaps because of the idea of ​​bypassing the technology patent, the domestic breakthrough in power cell energy density is to develop high-nickel cathode material NCM. The work of this piece is mainly promoted by the supplier of cathode materials, such as the domestic cathode material leader Shanshan. Although the current NCE811 material with the highest energy density in China has reached the level of 200mAh, it has not yet become commercialized.

In the face of higher energy density indicators in the future, perhaps NCM can do nothing. To this end, domestic power battery companies are developing solid-state batteries and lithium metal batteries with higher energy density. Ningde era claimed last year that it has carried out lithium metal batteries with lithium as a negative electrode material (the theoretical energy density of lithium is currently 10 times that of mainstream graphite), and solid electrolyte batteries with solid electrolytes. These techniques will spur the energy density of the individual cells to a target of 500 Wh/g.

Conclusion: Power battery moves from chaos to order

Looking back at the development of the domestic power battery industry in these years, it can be clearly found that "the blindfolded madness" is a true portrayal of this new industry. Whether it is a fraudulent incident or a overcapacity on the fast-drying, it is the price paid for the rapid development.

But after years of blindfolding, the situation is changing.

The power battery industry, which has entered the post-subsidy era from the subsidy era, is establishing order from the chaos of the masses. The speed of the battery giant beast in Ningde era has already released a clear signal - the domestic power battery company The era of great integration is approaching.

The first spokesperson to build a new order has been born, and the ruling objects in the process of establishing the new order, the small players who want to beat the temper, leave them with a small window of time.

*Note: In terms of the total installed capacity of power batteries, the statistics of different statistical calibers are slightly different, but they are the same in the industry rankings. For the convenience of discussion, the first electric data is used in the data of "power battery installed capacity".

Wall charger is AC/DC Adapter, which plugs into home Socket directly to use, no need to connect another Cable , it has EU plug, US plug, UK plug, AUS plug, Brasil Plug and Argentina Plug, used in different countries. Wall adapter is widely used for mobile phone, tablet, pos machine, modem, led light, cctv camera, DVD, router, and other small home devices.

The normal output voltage of wall plug adapter is 5V, 9V, 12V, 24V, but yidashun can do any voltage like 8V, 15V, 18V, 22V and so on, the maximum power is 48W. And the DC Cable of wall mount adapter is 1.2m normally, but yidashun can do 1.5m, 1.8m, 2m, 3m and longer as you want, so any customized wall plug in adapter is welcome!

Wall Charger,USB Wall Adapter,Portable Wall Charger,Wall Mount Adapter

Shenzhen Yidashun Technology Co., Ltd. , https://www.ydsadapter.com