Historical Changes and Future Trends of China's New Energy Costs

The sustainable development of new energy needs to rely on its own technological progress and cost reduction, reduce the dependence on subsidies, the country also proposed the wind power in the power generation side to parity access to the Internet in 2020, photovoltaic power generation at the user side of the goal of parity Internet access. Based on the analysis of the historical changes in the cost of China's new energy generation and future cost trends, we forecast the cost of new energy generation in China in 2020 and 2030, and analyze the situation of future cheap prices. The results show that by 2020, wind power in the “Three North†region will be basically realized. On the power generation side, parity Internet access and east-central photovoltaic power generation are used at the user's side for parity access. In 2030, the average cost of photovoltaic power generation is expected to be lower than that of wind power.

introduction

In recent years, the rapid development of new energy in China has made greater contributions to the adjustment of energy structure. As of the end of 2016, the cumulative installed capacity of wind power was 149 million kW, which became the third largest power source after coal power and hydropower. The cumulative installed capacity of photovoltaic power generation was 77.42 million kW, which together accounted for 14% of the country's total installed capacity of electricity. In the first half of 2017, new energy sources still maintained a rapid development momentum. Wind power and photovoltaic power generation increased by 4.91 million and 24.4 million kW, respectively. It is expected that by the end of 2017, cumulative installed capacity of wind power and photovoltaic power generation will exceed 290 million kW. While making great achievements in new energy development, it also needs urgent attention to solve some problems: On the one hand, how to enhance the endogenous driving force of new energy industries and increase the competitiveness of equal participation in the market; on the other hand, existing subsidy policies have promoted the rapid development of the industry. However, it is also faced with the difficulty of increasing the shortfall of subsidy funds year by year, affecting sustainable development. Therefore, this article analyzes the historical changes and future trends of China's new energy generation costs and related external costs, and puts forward relevant policy recommendations.

1. Global new energy generation cost

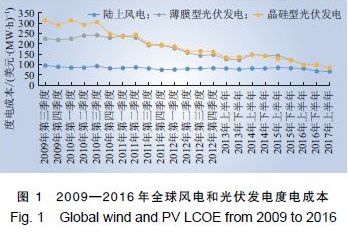

The cost of wind power and photovoltaic power generation continues to decline worldwide. According to Bloomberg New Energy Financial Data, the average cost of onshore wind power in the second half of 2016 was 18% lower than that in the second half of 2015, and photovoltaic power generation was down 17%. The main reason was that prices of key equipment such as wind turbines, photovoltaic modules, and inverters decreased. And project development experience has gradually matured. Figure 1 shows the cost of global wind power and photovoltaic electricity generation during 2009-2016.

In order to encourage new energy generation to reduce costs, at least 67 countries around the world have adopted bidding methods to determine on-grid tariffs. According to the statistics of the International Renewable Energy Agency (IRENA), the global bid price of wind power and photovoltaic power generation in 2016 was 0.20~0.46 yuan/(kW ̇h) and 0.16~0.80 yuan/(kW·h) respectively.

2. Historical changes and future trends of China's new energy costs

2.1 Changes in China's New Energy Generation Costs

2.1.1 Wind power costs

In recent years, the entire industrial chain of wind power in China has gradually become localized, and the technical level and reliability of wind power equipment have been continuously improved. The overall cost of wind farms has been declining year by year. In 2015, the national wind power unit cost was reduced by 10% compared to 2012, as shown in Table 1. Show. As far as the specific types are concerned, the unit cost of decentralized wind power projects is higher than that of large-scale wind farms, mainly due to the high unit price of wind turbines and the weak scale of the project.

With the adjustment of wind power layout in 2016, the newly installed capacity in the eastern and southern regions accounted for 44% of the total new increase in the country, an increase of 11% compared with the same period of last year. The statistics included Sichuan, Chongqing, Shandong, Henan and other provinces. The higher level makes the average cost of wind power in 2016 as 8 157 yuan/kW, slightly more than 2015.

From the perspective of regional differences, the average unit cost of wind power in the “Three North†region is lower than that in the eastern and central regions. The main reasons are: First, differences in construction conditions. Wind power in the central and eastern regions is mainly built on mountainous terrain and coastal beaches, with poor geological conditions and transportation infrastructure. The cost of wind turbine infrastructure and road traffic engineering is relatively high. Second, the difference in land costs, the shortage of land resources in the eastern region, and the acquisition of wind power land indicators are difficult and costly.

According to Bloomberg New Energy Finance data, the average national wind power cost in 2016 is about 0.5 yuan/(kW·h), which is still higher than the benchmark price of coal (0.25~0.45 yuan/(kW·h)).

Photovoltaic cost

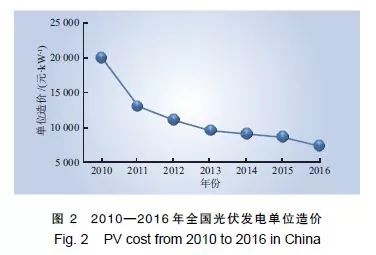

With the technological advancement of photovoltaic power generation, industrial upgrading and market expansion, the cost of China's photovoltaic power generation has continued to decline. The unit capacity cost has dropped from about 20 000 yuan/kW in 2010 to about 7 000 yuan/kW in 2016 (see Figure 2). ). In terms of specific types, the cost of distributed photovoltaic power generation is 10%~20% higher than that of photovoltaic power plants.

According to the data of Bloomberg New Energy Finance, the national photovoltaic power generation cost fluctuation range in 2016 was relatively large, ranging from 0.55 to 1.02 yuan/(kW·h) with an average of 0.68 yuan/(kW·h).

2.2 Trends and Comparative Analysis of Future Costs of China's New Energy

2.2.1 Future Cost Trends of China's New Energy Generation

The decline in the cost of future wind power projects will mainly depend on the decline in the cost of key equipment and non-technical costs. The former mainly depends on technological progress and the selection of wind turbines. The latter mainly consists of land fees and taxes. According to GE's research results, technical breakthroughs such as longer and lighter blades and integrated transmission chains will reduce wind power cost by 0.050 to 0.067 yuan/(kW·h) in 2025. The optimal design of micro-site selection and fan selection will be implemented. The cost of electricity is reduced by 0.031~0.070 yuan/(kW·h).

With reference to the average annual decline in the unit cost of wind power projects in the subregion in 2012–2015, forecasted by 2015 constant prices, the unit cost of wind power projects nationwide in 2020 is approximately RMB 6 700/kW (see Table 2), and is approximately 4 600 in 2030. Yuan/kW.

Photovoltaic power generation unit capacity still has great potential for decline in the near to mid-term, mainly due to the declining trend of non-technical costs such as photovoltaic modules, inverters, and land costs, taxes and fees. Among them, the decrease in the cost of photovoltaic modules mainly depends on the decrease in the cost of silicon materials, the improvement of the conversion efficiency of the modules, and the improvement in the utilization of silicon.

Combined with the analysis of the trend of key indicators of the PV module industry by the China Photovoltaic Industry Association, the forecast is based on the 2015 constant price: The national PV power generation unit capacity cost will be approximately 5 500 yuan/kW in 2020, and approximately 3 000 yuan/kW in 2030. Among them, in Central China, Northeast China, South China, East China, North China, and Northwest China, 2020 were 5 655, 5 740, 5 655, 5 486, 5 318, and 5148 yuan/kW, respectively.

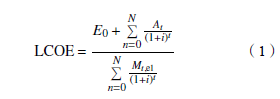

In order to facilitate the comparison with the benchmark price, the concept of leveled cost of electricity (LCOE) is also commonly referred to as the cost of electricity. Equalization power generation cost refers to the comprehensive cost of power generated by the power generation project, that is, the ratio of all costs generated by the power generation project during the entire operation period to the total power generation. The formula is:

In the formula: LCOE is the levelization of power generation cost; At is the operating expenditure of the t year; E0 is the initial investment of the project; i is the investment return rate; Mt, el is the power generation amount of the year; n is the project life considered in the financial analysis t is the year the project was run (1,2,3,...,n).

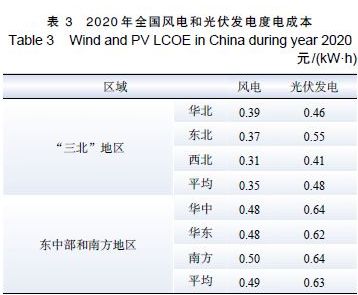

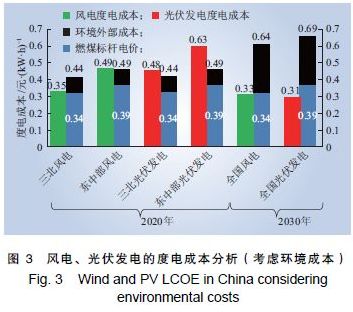

The calculation results are as follows: The average cost of wind power in the “Three North†region in 2020 is 0.35 yuan/(kW ̇h), which is lower than that in the eastern central region (0.49 yuan/(kW•h)); the average of photovoltaic power generation in the “Three North†region The electricity cost is 0.48 yuan/(kW·h), which is lower than the cost of photovoltaic power generation in the eastern and central regions (0.63 yuan/(kW·h)) (see Table 3). In 2030, the average cost of wind power in the country fell to 0.33 yuan/(kW·h), and the average electricity cost of photovoltaic power generation was 0.31 yuan/(kW·h).

2.2.2 Contrast Analysis of Electricity Price on Generation Side and User Side

According to the “13th Five-Year Plan for Renewable Energy Developmentâ€, by 2020, the price of wind power projects can compete with the local coal-fired power generation platform, and the electricity price of photovoltaic power generation projects can be equivalent to the sales price of power grids. The forecasted 2020 and 2030 wind power and photovoltaic power generation cost will be compared with the power generation side and user side electricity prices (only considering the new energy self-generation cost and not considering the environmental external costs). The results are as follows.

(1) Contrast with the local coal-fired benchmark price and the grid sales price. In 2020, wind power in most provinces in the “Three North†region can achieve grid-connected access to electricity at the power generation side, but the price of coal-fired benchmarks in Gansu, Ningxia, Inner Mongolia and other provinces is relatively low. It is difficult for wind power to achieve grid parity at the power generation side, and wind power in the eastern and central regions is still difficult to generate electricity. Side-to-price Internet access; Photovoltaic power generation in the eastern and central regions can basically achieve user-side (large-scale industrial users and general industrial and commercial users) access to the Internet at a low price, and photovoltaic power generation in the “Three North†region is still difficult to achieve user-side parity access. In 2030, photovoltaic power generation cost will be lower than wind power, and it will be more competitive.

(2) Comparison of the transfer of new energy generation across regions in the "Three North" area and the replacement of new energy development in the eastern and central regions. When the abandonment rate of abandoned wind is controlled at a reasonable level, the prices of wind power and photovoltaic power generation sent to the eastern and central regions in the “Three North†region will be about 0.61, 0.75 yuan/(kW·h) in 2020, respectively. The development of consumption in the central region is more economical in the province. The price of the latter is about 0.65, 0.79 yuan/(kW·h) respectively.

(3) Comparison of cross-regional delivery of new energy power generation in the “Three North†region and coal power in the eastern and central regions. Considering only the extra high-voltage drop-off points sent to the eastern and central regions, the price of wind power transmission across the “three north†regions will reach around 0.40 yuan/(kW·h) in 2020, and the cost of 500 kV transmission will exceed most of the cost. The price of coal-fired benchmarks in the eastern and central provinces is relatively poor. According to the existing trans-regional transmission transmission prices, the average transmission and distribution price in the east and the middle, and the number of hours of power generation based on resource conditions, it is expected that the price of photovoltaic power generation in the “Three North†region will be sent to the East China Tribes more than that in the East Central China. Coal-fired electricity prices are higher.

2.2.3 Comparative Analysis After Considering Environmental Costs and System Costs

Considering the new energy's own power generation cost and the external cost of coal-fired power generation environment, referring to the research results of Greenpeace International, the external costs of coal-fired power generation environment include the pollution emission and carbon emissions of coal-fired power generation, coal production and transportation links to the environment. The negative impact, etc., in 2020 and 2030 were 0.095 and 0.300 1 yuan/(kW·h), respectively. According to a comprehensive analysis, in 2020, the wind power in the East Central and “Three North†photovoltaic power generation could also initially compete with the coal-fired power generation platform. In 2030, the competitive advantage of wind power and photovoltaic power generation in the country will be more apparent (see Figure 3).

In addition, the development of new energy not only needs to pay attention to the cost of its own power generation, but also pay attention to the cost of the system. Compared with conventional power supplies, large-scale grid-connected new energy will inevitably increase the system's balance costs and capacity costs. Wind power and other volatile power output fluctuations, the need for power systems to provide peaking, FM, standby and other ancillary services, increase the balance of costs. Wind power and other volatile power sources have low reliability and need to provide spare capacity to increase the capacity surplus cost. According to the results of the IEA study, when the wind power ratio reached 20%, the balance cost and capacity adequacy costs were 1 to 7 US$/(kW·h) and 4 to 5 US$/(kW·h), respectively.

Considering that China belongs to the continental monsoon climate, wind power output is lower than Europe and the United States, the overall prediction accuracy of new energy power generation is still insufficient, and the proportion of coal and electricity is high, the additional system cost caused by new energy in China is higher than in Europe and the United States.

Based on the above content analysis, the following three perspectives are drawn.

(1) The cost of wind power and photovoltaic power generation still has a large space for decline. In 2020, basically the wind power in the “Three North†region will be connected to the grid at the power generation side and the eastern and central photovoltaic power generation will be accessed at the user’s side.

(2) In the medium and long term, photovoltaic power generation has more space to fall than wind power. In 2030, the average power cost of photovoltaic power generation is expected to be lower than that of wind power. With the abandonment of wind and abandoned light at a reasonable level, wind power and photovoltaic power generation in the “Three North†region will span. The district is sent to the eastern and central regions and is more economical than the new energy development in the eastern and central regions. To achieve the long-term goals for the development of new energy resources, we must rely on the “Three North†region and the western region.

(3) New energy power generation such as wind power and photovoltaic power generation not only needs to pay attention to its own power generation cost, but also need to pay attention to the additional system cost brought to the entire power system, mainly including balance cost and capacity aptitude cost.

3. Sustainable Development of China's New Energy

3.1 International New Energy Support Policies and Implications

Given the differences in energy transformation requirements, policy frameworks, and market models, there are differences in the new energy support policies of different countries. On the whole, at present, most countries use the fixed price of electricity (FIT) and reward + market price mechanism (FIP).

Danish incentive policies are effective. Denmark has adopted policies including carbon taxation, carbon emission quotas, environmental protection taxes, on-grid tariff subsidies, R&D subsidies, infrastructure construction, and wind power industry support to promote wind power development. In the early days, Denmark used the installation fund and electricity price subsidy to require new energy resources to be given priority access to the Internet. Later, it used fixed on-grid tariffs and subsidies for subsidy as the main support means.

Spanish price incentives "dual track system." Renewable Energy Power The Internet adopts a "dual track system". Under the “policy trackâ€, the basic income of renewable energy power generation enterprises is guaranteed through a fixed electricity price support policy; under the “market trackâ€, renewable energy power generation enterprises are encouraged to participate more in market competition under the basic guarantee of fixed electricity price policies, and obtain Additional income.

The United States establishes a sound taxation policy and actively promotes the quota system. The related tax policies of the new energy industry in the United States run through the production and consumption sectors of the industry. The United States is the first country to implement a quota system (RPS). At present, 29 states have established and implemented renewable energy quota systems.

Germany adjusted its support policy in a timely manner in accordance with the development stage of renewable energy. The first edition of the Renewable Energy Law, EEG 2000, established an incentive policy system based on fixed on-grid electricity prices. Renewable energy generation entered the initial stage. The EEG 2004 edition further improved the on-grid tariff policy and introduced a fixed down-regulation mechanism for on-grid tariffs. Renewable energy generation entered a phase of rapid development. The EEG 2009 edition establishes a fixed on-grid tariff reduction mechanism based on newly installed capacity, and encourages self-use through subsidies. During this period, the investment cost of photovoltaic power generation dropped drastically, and the reduction in on-grid electricity prices did not keep pace with the rapid growth of photovoltaic power generation. The EEG 2012 edition further improved the fixed on-grid tariff reduction mechanism based on newly installed capacity, increased the frequency of cuts, encouraged renewable energy generation to enter the market, and also incorporated small-scale photovoltaic power generation into the system monitoring range. For the first time, the EEG 2014 edition proposed to determine the PV subsidy quota through bidding, further promote the marketization of photovoltaic power generation based on the market premium mechanism, and reduce and gradually withdraw subsidies. EEG 2017 fully introduced the tendering system for renewable energy power generation, formally ended the government pricing mechanism based on fixed on-grid tariffs, and comprehensively promoted the marketization of renewable energy power generation. This revision is in response to the European Union's requirements for renewable energy support policies in various countries, as well as the intrinsic motivation for realizing renewable energy development goals and reducing development costs.

Based on the comprehensive analysis, the following three implications are drawn.

(1) In the initial stage of new energy development, it is necessary to rely on subsidies in various ways to achieve mutual promotion of scale expansion and cost reduction, and to enhance industrial competitiveness, but it should not rely on subsidies for a long time. All countries have adopted a policy of gradual reduction and elimination of subsidies in accordance with their national conditions, the process of energy transformation goals and their own endurance.

(2) The introduction of market mechanisms can promote the sustainable development of new energy. Through the tendering system to achieve competition in the development of investment rights, forced to reduce costs; due to the lower marginal cost of new energy generation, in the fully competitive market mechanism can rely on its cost advantage to ensure priority scheduling, promote the priority of new energy consumption.

(3) The quota system can play an important role in the case of imperfect electricity markets across provinces and regions, and gradually increase the quota requirements to promote new energy consumption in a wider range.

3.2 Problems to be Solved in the Sustainable Development of New Energy in China

Since the “Eleventh Five-Year Plan†period, China has gradually established a new energy policy system that covers on-grid tariffs, full-scale guaranteed acquisitions, subsidy funds, and tax incentives, which has promoted the rapid development of new energy sources, but has also caused some problems. attention.

(1) The high intensity of subsidies and the large gap in subsidies make it difficult to sustain. The intensity of new energy subsidies in China is high. In 2016, the subsidy strengths of wind power and photovoltaic power generation are approximately 0.17 and 0.53 yuan/(kW·h) respectively. As of the end of 2016, the cumulative funding gap for subsidies exceeded RMB 55 billion. If the existing policy is maintained (regardless of CSP and grid-connected subsidies, and according to the current fund collection ratio), the accumulated gap in the renewable energy development fund during the “13th Five-Year Plan†period is expected to reach RMB 200 billion.

(2) The current price mechanism does not play a significant role in reducing costs and promoting consumption. In recent years, the cost of new energy power generation, especially photovoltaic power generation, has fallen by a large margin. However, policy adjustments have lagged behind. The reduction in benchmark power prices has lags behind the cost reduction, and the limited scale determined by market competition has led developers to reduce their own costs. insufficient. In addition, the current pricing mechanism based on the benchmark price only stimulates new energy developers, but lacks incentives for regular power compensation adjustments.

(3) The lack of research on system costs and countermeasures caused by new energy sources has caused insufficient incentives for related parties. New energy has characteristics such as randomness and intermittency, low trustworthy capacity, power system must be equipped with enough flexible power supplies, which brings additional balance costs and capacity adequacy costs, etc. At present, the research on the cost of these systems is not enough, and the lack thereof. Compensation Mechanism. At present, China is exploring the establishment of relevant marketization mechanisms, but little progress has been made. For example, pilots of clean energy alternatives to captive power plants have only been implemented in the northwestern region, and piloting of ancillary services is limited to the Northeast, Xinjiang, and Fujian.

4 Conclusion

The analysis shows that in 2020, wind power in most provinces in the “Three North†region can realize grid parity at the power generation side. Photovoltaic power generation in the eastern and central regions can basically achieve user-side (large-scale industrial users and general industrial and commercial users) parity access to the Internet. From the perspective of international experience, the sustainable development of new energy still needs to stimulate the endogenous driving force of the industry, promote technological progress and cost reduction, reduce the dependence on subsidies, and reduce the development costs. It is necessary to establish a force-reduction mechanism to achieve the desired goals of new energy development and integration into the large power grid. . By improving electricity price reduction mechanism, optimizing the layout of scale, reducing non-technical costs, and raising technical thresholds, etc., we will guide industrial upgrading and continuously upgrade the quality of new energy development. We will introduce market mechanisms in the development of capacity and on-grid power to encourage sharing of benefits with conventional power supplies. Efforts will be made to break provincial barriers, promote the absorption of new energy, and promote the transformation of China's energy system to a clean, low-carbon, and accelerated transition.

Biotept gear reducer

Biotept production and sales company of motor, reducer, step motor, servo motor, Helical Gear Reducer, variable frequency speed motor, hard tooth surface reducer, Brushless Motor, servo planetary reducer, direct axis reducer, three-phase asynchronous motor, worm and Worm Reducer for China and foreign markets.

It has achieved the same results in various manufacturing industries such as electronic equipment, printing machinery, packaging machinery, carton machinery, food machinery, zipper machinery, coating machinery, hardware machinery, manipulator, injection molding machine, woodworking machinery, cosmetics machinery, textile machinery, filling machinery and chemical machinery Be a good market share.

NMRW worm reducer

VF worm gear reducer

KM helical-hypoid gear reducer

BKM helical-hypoid gear reducer

MRC helical gear reducer

FC parallel shaft helical gear reducer

RC in-line helical gear reducer

KC helical-bevel gear reducer

SC helical-worm gear reducer

HB heavy duty gearbox

HB heavy duty gearbox

Gear Box,Bevel Gearbox,Gear Boxes,Small Gearbox

Ningbo Biote Mechanical Electrical Co.,Ltd , https://www.biotept.com